Eggstack is an independent financial technology company located in Jacksonville, Florida. Our mission is to help you overcome uncertainty about retirement planning and inspire confidence in your financial future.

Did you know the average American spends about 20% of their income on vehicles? That includes purchase (or lease), insurance, fuel, maintenance, repairs, depreciation, taxes, and fees. What if you could cut that number in half? By downsizing to one car in retirement, that is exactly what you would be doing.

Retirement brings many changes, and for those who work outside the home, it means no more daily commute. When you and your spouse or partner retire, you may be able to downsize to one car.

If you are already retired, it’s pretty simple to determine if this might be right for you. If both of your vehicles are rarely used at the same time, becoming a one-car household should be fairly easy.

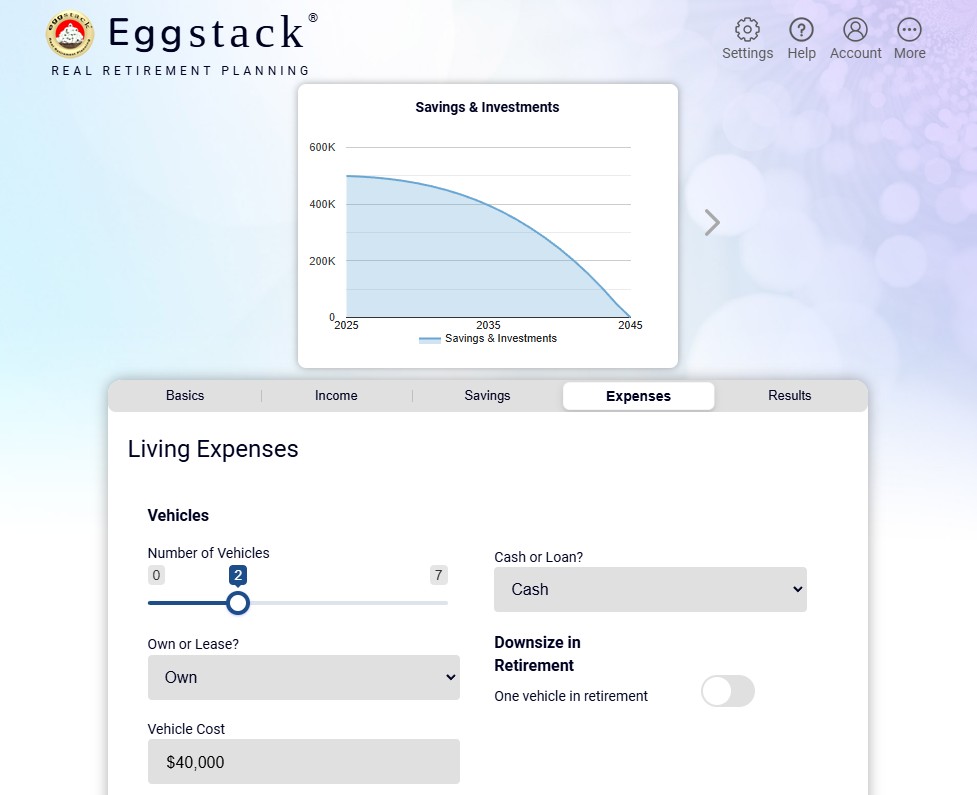

To get a feel for whether downsizing to one car is worth it, let’s use Eggstack to do a quick analysis. Our example is based on a newly-retired middle-class couple with $500,000 in retirement savings. They are 65 years old and expect to live another 20 years. Each vehicle is traded in every 10 years on a new model priced at an inflation-adjusted $40,000.

As shown in the image below, with two cars throughout retirement our couple runs out of money right at plan end. That means if the slightest thing goes wrong, they will outlive their savings.

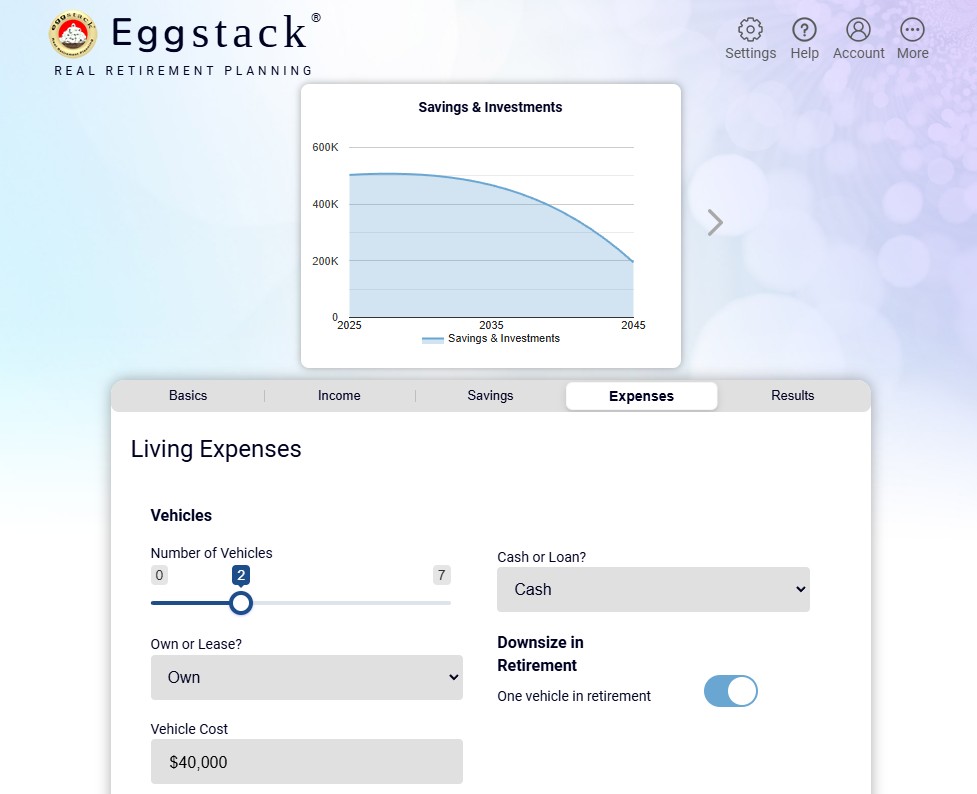

Now, keeping everything else the same, let’s see what happens if the same couple downsizes to one car in retirement. By clicking Downsize to One Vehicle in Retirement, Eggstack automatically changes the analysis to model retirement with one vehicle. You can see the difference in the image below.

By only having only one car in retirement, our couple has $200,000 leftover at plan end. That’s peace of mind. That’s a secure retirement. If there are some bumps along the way – and there will be – our couple will have the extra cash they need.

Downsizing to one car in retirement can definitely make your retirement savings last longer. However, it might not be practical for some couples. Here are some examples of situations where downsizing to one car might not be a good idea.

Downsizing Nonstarters

Another consideration is taking your car to the shop. With two vehicles, your significant other can follow you and bring you back home. If you have only one car, you’re looking at taking an Uber, phoning a friend, or sitting there until your car is finished.

There is a measure of inconvenience that comes with owning only one vehicle. Your freedom to come and go is hampered. You and your better half may need to establish a “car calendar" – a joint calendar for appointments and other commitments that require the car. This will help avoid scheduling conflicts.

Another idea is what could be considered a “hybrid" approach – a compromise between owning one car and two. Your second vehicle could be a “beater car." If you are unfamiliar with the term, think older, mostly used up – something a college kid might drive. It solves the issues of freedom and convenience, while still reducing your vehicle costs. For example, a 15-year-old Honda Civic with 150,000 miles has pretty much depreciated all it ever will. Depreciation is by far the biggest cost of owning new vehicles. However, you will still have to insure two vehicles, which isn't cheap. Also, the beater car will likely need more repairs than a newer vehicle.

Conclusion

There is a lot to think about. Hopefully, we've given you some things to consider. Downsizing to one car in retirement is a big decision. However, it’s not irreversible – it’s not like jumping off a cliff. If you try it and it doesn’t work, you can just go buy another vehicle.

Photo credit: Pixabay Eggstack News will never post an article influenced by an outside company or advertiser. Our mission is to help you overcome uncertainty about retirement planning and inspire confidence in your financial future. This article is for informational purposes only and is not financial advice or any other type of advice. Eggstack makes no representation to the validity, accuracy, completeness, or suitability of purpose of any information presented in this article.